Encourage your employees to pursue accreditations in their different area of expertises; it will help your company's profile and obviously it will help the people. You can select to totally or partly sponsor a few of the accreditations tests. Finally, you need to keep your doors open for recommendations from members of your team and your clients.

Founder/ Publisher at Profitable Endeavor Publication LtdAjaero Tony Martins is a Business Owner, Realty Designer and Financier; with an enthusiasm for sharing his knowledge with budding business owners. He is the Executive Manufacturer @JanellaTV and likewise functions as the CEO, POJAS Characteristics Ltd. Most current posts by Ajaero Tony Martins (see all).

Buying a Shell Could be a Smart Move for Some Profit-Seeking Brokers Oft times, handling basic representatives, wholesalers and insurance brokers feel they are improperly compensated for the essential services they offer in proportion to the substantial revenues they see going to their providers or fronting companies from their book of organization.

Typically, providers and fronting business charge significant fronting costs, upwards of 6-10 percent, for the use of their scores, licenses, admitted/non-admitted paper, etc. Brokers follow this link with great underwriting (i. e. low loss ratios) can not assist however drool at the thought of eliminating these heavy fronting fees and combining the savings with the substantial revenues potential they could understand by maintaining the threat themselves.

Probably the most common approach is by method of revenue sharing commissions with carriers. Nevertheless, this restricts the broker to only taking a small part of revenue. The next action up is likely some kind of quota share arrangement in between the broker and the carrier in which the broker accepts assume a portion of the threat, backed by a letter of credit (which ties up capital), in exchange for a portion of the earnings.

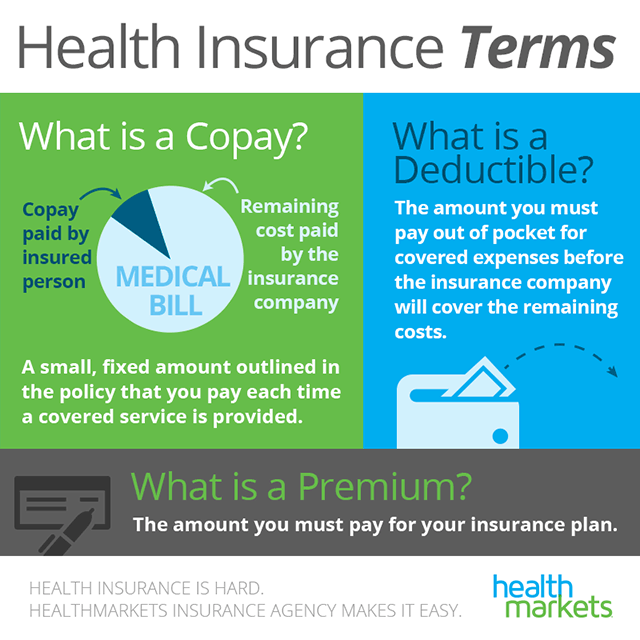

9 Simple Techniques For How Do I Get Health Insurance

The only method for a brokerage to catch all the profit is to establish its own insurance provider. If successful, this act makes it possible for the brokerage company to "manage its own destiny." To do this is no easy task, but it is possible. The key is in knowing precisely what is at stake and understanding all the aspects that need to remain in location before proceeding.

Lots of additional things should be thought about, implemented and achieved before an effective start-up can be realized. The choices to be made are seemingly endless and begin with the geographic footprint preferred, where the company should be domiciled, and statutory surplus requirements of the states included. Additionally, the complexities associated with getting a charter, the multi state regulatory approvals processes and attaining the A.M.

Collectively, these challenges, and much more, provide a drain on a broker's time, resources and the capability to run the daily service. who is https://gregoryuhsv099.skyrock.com/3337476236-How-How-To-Get-A-Breast-Pump-Through-Insurance-can-Save-You-Time.html eligible for usaa insurance. Fortunately, there is a typically utilized shortcut which prevents some of the problems associated with beginning an insurer. A number of early hurdles may be cleared by just purchasing among the lots of shell insurance companies on the marketplace today.

This is an insurer with licenses however without old insurance coverage liabilities or legacies. Acquiring a shell will not get rid of vital choices such where to domicile or in which states are licenses required. Nor will it guarantee the needed A. M. Best rating or state regulatory approval of the new ownership.

Shells in today's market are numerous, but there are significant entry costs. The seller of the shell will desire 2 things: 1) A dollar for dollar exchange for delivering the shell to the purchaser with the capital bound in Find more info the shell. Some shells are accompanied with as little as $2 million in capital and surplus.

The 6-Second Trick For How Much Does Insurance Go Up After An Accident

For instance, if the shell has current capital and surplus of $5 million and is licensed in 10 states, the buyer will require to provide $5. 5 million to the seller at closing. This presumes that the seller will sell the licenses for $50,000 per state. The rate spent for a license depends upon the number of licenses brought by the shell, and, of course, where the shell is certified to write company.

Normally license costs are in direct proportion to the population of the state (how do insurance companies make money). The most pricey shells are those certified in all or many of the 50 states and the District of Columbia. Over the past 9 months, the rates of these licenses have been, usually, $139,233 and as high as $250,000.

What else should be thought about when acquiring a shell? Initially, it is very important to comprehend that some states have minimum capital requirements. Rankings from A.M. Finest are also a key concern. A company unable to get the proper score may not have the ability to compose business straight and rather needs to settle on a fronting carrier.

Likewise, how much extra capital is required to support the new company that goes into the shell? What levels of net composed premiums to surplus ratio must be preserved going forward? If you can bring significant premium volume, perhaps a big capital raise from a private equity group is worth checking out - how to get rid of mortgage insurance.

The factors to consider can be intimidating unless the buyer fully comprehends the procedure. If this knowledge is not available in house, the broker would be smart to employ a consultant that has been through the procedure, comprehends the regulative issues and comprehends capital and ratings requirements. In the event begin up capital may not be easily available, there are methods to obtain this funding.

The Best Guide To How To Get Health Insurance After Open Enrollment

Access to capital will depend on the broker's success record, the strength of management, business strategy and the amount needed along with the appropriate relationships with financiers. Carrying out the start up of an insurance company, although daunting, is not an insurmountable goal for brokers who are certified, capitalized and well encouraged.

Laughton Sherman (LSherman@LMC Capital. com) is managing director of LMC Capital LLC, a nationwide financial investment banking company dedicated exclusively to the insurance coverage market. Among other services, LMC supplies industry-specific guidance as it relates to the sale of brokers/agencies, mergers and acquisitions, debt financing, evaluations, and/or evaluating strategic options. The company is situated in Charlotte, N.C.

So, you're considering opening your own insurance coverage agency ?! Well, before you unlock for the very first time, a review of the laws and guidelines affecting insurance agents and the operation of Florida companies could be really helpful to you. After all, you wish to preserve a certified company.

Here's a fast summary of the laws and procedures that brand-new (and not-so-new) agents frequently ask about, along with the appropriate legal citations, for opening a major * lines insurance company. If that's not for you, make sure to examine out the guidelines for opening title insurance coverage agencies and bail bond agencies.

Florida law avoids you from naming your firm anything that would be deceptive or deceptive in any method. Names chosen must not suggest that the firm is an insurance provider, governmental agency, or any other nationwide or state organization. We will not permit any agency to use a name that does not satisfy this criteria.